Note

Go to the end to download the full example code.

Consumption-Saving-Portfolio Model¶

The consumption-saving problem is one of the central models of modern macroeconomics and household finance. An agent with uncertain income must decide each period how much to consume and how much to save, trading off current utility against future resources.

This example uses the model blocks defined in

skagent.models.consumer, which implements Carroll’s (2001) [1]

formulation of the normalized buffer-stock problem and extends it with a

portfolio choice between a safe bond and a risky asset.

Model Structure¶

The model is built from three composable blocks:

consumption_block_normalized- one period of the normalized consumption-saving problemportfolio_block- risky portfolio allocation that endogenizes the gross return \(R\)tick_block- state transition that carries end-of-period assets into next period’s capital

The two complete recursive problems are:

cons_problem- pure saving (fixed return)cons_portfolio_problem- saving plus portfolio choice

Normalized Consumption Block¶

State Variable: \(k_t\) - normalized capital (assets divided by permanent income) carried into the period

Shocks:

\(\theta_t\) - transitory income shock, \(\mathbb{E}[\theta_t] = 1\)

Dynamics:

where \(G\) = PermGroFac is the permanent income growth factor and

\(R\) is the gross return on savings.

Utility:

Portfolio Block¶

The portfolio block augments the saving problem with an endogenous asset return. The agent chooses the risky share \(\varsigma_t \in [0,1]\):

where \(R^{\text{risky}}_t \sim \text{Lognormal}(R_f + \text{EqP},\, \text{RiskyStd})\).

Parameters¶

\(\beta\) (

DiscFac) = 0.96: Discount factor\(\rho\) (

CRRA) = 2.0: Coefficient of relative risk aversion\(R\) = 1.03: Gross safe return (3 % per period)

\(G\) (

PermGroFac) = 1.01: Permanent income growth factor\(\sigma_\theta\) (

TranShkStd) = 0.1: Transitory income shock std\(R_f\) (

Rfree) = 1.03: Risk-free rate\(\text{EqP}\) = 0.02: Equity premium

\(\sigma_R\) (

RiskyStd) = 0.1: Risky return std

References¶

import matplotlib.pyplot as plt

import numpy as np

import skagent as ska

from skagent.distributions import Normal

import skagent.models.consumer as cons

Model Inspection¶

Load the predefined model elements and inspect them.

Step 1: Show Model Parameters¶

print("Model Calibration:")

for param, value in cons.calibration.items():

print(f" {param}: {value}")

Model Calibration:

DiscFac: 0.96

CRRA: 2.0

R: 1.03

Rfree: 1.03

EqP: 0.02

LivPrb: 0.98

PermGroFac: 1.01

TranShkStd: 0.1

RiskyStd: 0.1

kInitStd: 1

pInitStd: 1

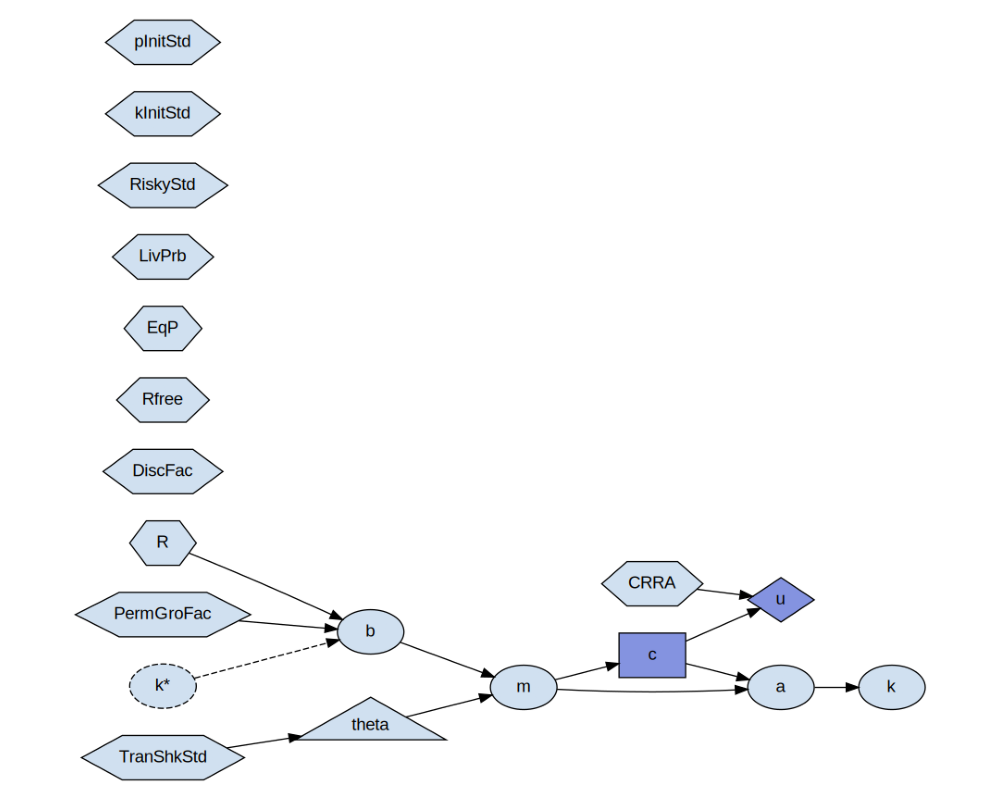

Step 2a: Inspect the Consumption Block Formulas¶

cons.cons_problem.display_formulas()

b = lambda k, R, PermGroFac: k * R / PermGroFac

m = lambda b, theta: b + theta

c = Control(m)

a = lambda m, c: m - c

u = lambda c, CRRA: torch.log(c

k = lambda a: a

Step 2b: Visualize the Consumption Block¶

img, _ = cons.cons_problem.display(cons.calibration)

plt.figure(figsize=(10, 8))

plt.imshow(img)

plt.axis("off")

plt.tight_layout()

<IPython.core.display.SVG object>

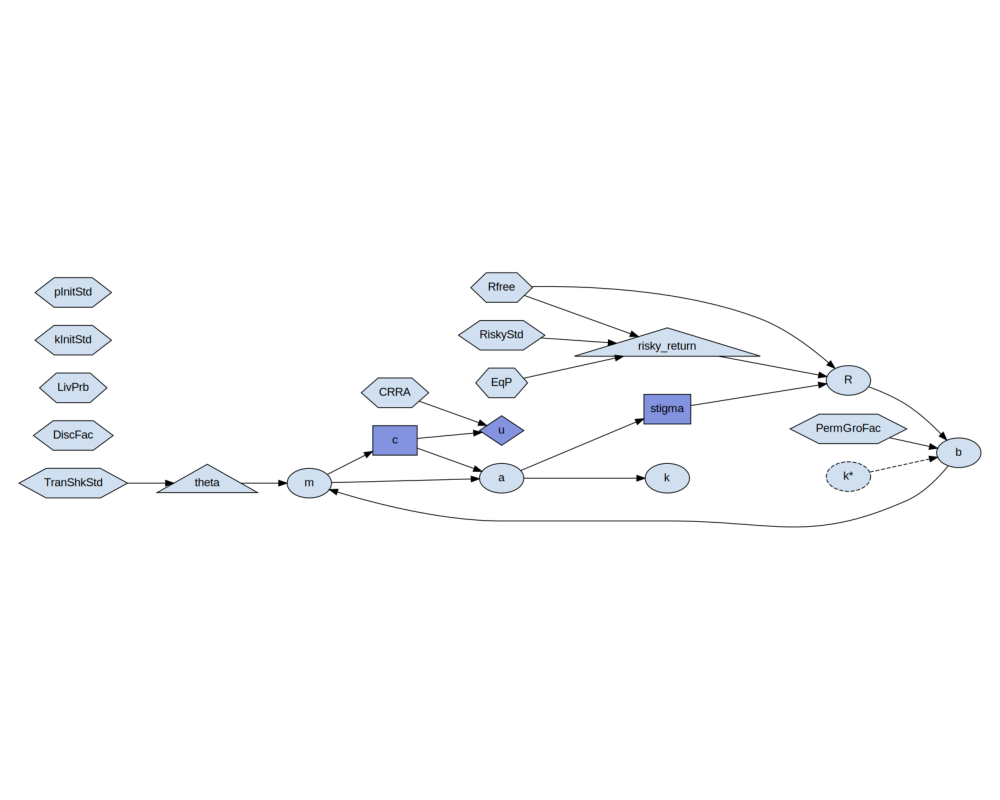

Step 3a: Inspect and visualize the Portfolio Block¶

cons.cons_portfolio_problem.display_formulas()

b = lambda k, R, PermGroFac: k * R / PermGroFac

m = lambda b, theta: b + theta

c = Control(m)

a = lambda m, c: m - c

u = lambda c, CRRA: torch.log(c

stigma = Control(a)

R = lambda stigma, Rfree, risky_return: Rfree

k = lambda a: a

Step 3b: Inspect and visualize the Portfolio Block¶

img, _ = cons.cons_portfolio_problem.display(cons.calibration)

plt.figure(figsize=(10, 8))

plt.imshow(img)

plt.axis("off")

plt.tight_layout()

<IPython.core.display.SVG object>

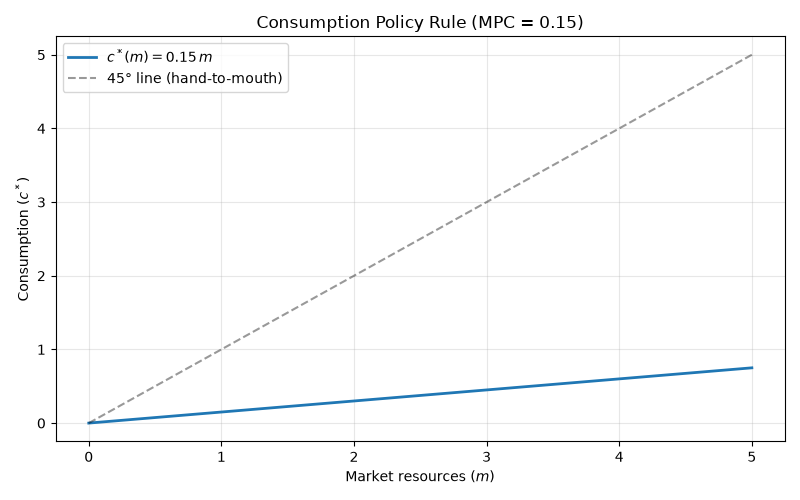

Step 4: Define a Simple Consumption Rule¶

The optimal policy for this model requires numerical solution methods. Here we use a simple constant marginal propensity to consume (MPC) rule as a tractable approximation:

where \(\kappa \in (0, 1)\) is a fixed MPC. A low MPC creates buffer-stock saving behaviour: agents accumulate assets and consume out of wealth gradually.

MPC = 0.15 # Marginal propensity to consume

def consumption_rule(m):

"""Consume a fixed fraction of market resources each period."""

return MPC * m

decision_rule = {"c": consumption_rule}

# Plot the consumption rule

m_range = np.linspace(0, 5, 200)

plt.figure(figsize=(8, 5))

plt.plot(m_range, consumption_rule(m_range), linewidth=2, label=rf"$c^*(m) = {MPC}\,m$")

plt.plot(m_range, m_range, "k--", alpha=0.4, label="45° line (hand-to-mouth)")

plt.xlabel("Market resources ($m$)")

plt.ylabel("Consumption ($c^*$)")

plt.title(f"Consumption Policy Rule (MPC = {MPC})")

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

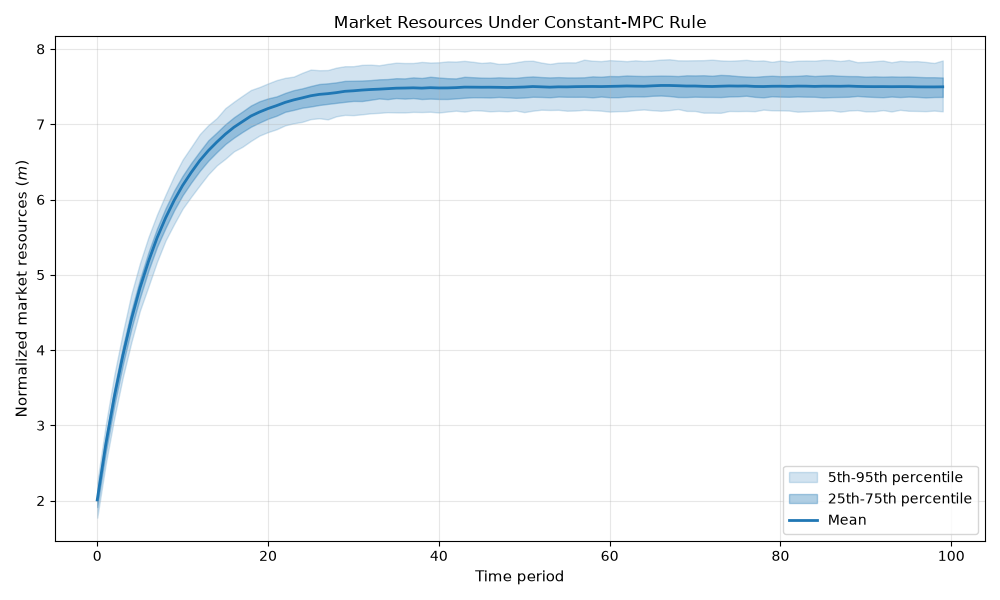

Step 5: Run Monte Carlo Simulation (Pure Saving Problem)¶

Simulate the pure saving problem (cons_problem)

which combines the normalized consumption block with the tick block.

Agents start with normalized capital \(k \approx 1\).

initial_conditions = {

"k": Normal(mu=1.0, sigma=0.1),

}

simulator = ska.MonteCarloSimulator(

calibration=cons.calibration.copy(),

block=cons.cons_problem,

dr=decision_rule,

initial=initial_conditions,

agent_count=1000,

T_sim=100,

seed=42,

)

print("\nRunning simulation...")

simulator.initialize_sim()

simulator.simulate()

print("Simulation completed successfully")

Running simulation...

Simulation completed successfully

Step 6: Plot Simulation Results¶

The plot shows the cross-sectional distribution of normalized market resources \(m_t\) over time. Under the constant-MPC rule, agents accumulate a buffer stock of savings that stabilizes around a long-run mean determined by \(\kappa\), \(R\), and \(G\).

plt.figure(figsize=(10, 6))

m_hist = simulator.history["m"]

plt.fill_between(

range(simulator.T_sim),

np.percentile(m_hist, 5, axis=1),

np.percentile(m_hist, 95, axis=1),

alpha=0.2,

color="C0",

label="5th-95th percentile",

)

plt.fill_between(

range(simulator.T_sim),

np.percentile(m_hist, 25, axis=1),

np.percentile(m_hist, 75, axis=1),

alpha=0.35,

color="C0",

label="25th-75th percentile",

)

plt.plot(m_hist.mean(axis=1), linewidth=2, color="C0", label="Mean")

plt.xlabel("Time period", fontsize=11)

plt.ylabel("Normalized market resources ($m$)", fontsize=11)

plt.title("Market Resources Under Constant-MPC Rule", fontsize=12)

plt.legend(fontsize=10)

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Step 7: Run Portfolio Simulation¶

Now extend to the portfolio problem

(cons_portfolio_problem),

where agents also choose their risky asset share \(\varsigma_t\).

We pair the MPC consumption rule with a fixed risky share of 0.5.

RISKY_SHARE = 0.5 # Fixed portfolio share in risky asset

portfolio_decision_rule = {

"c": consumption_rule,

"stigma": lambda a: RISKY_SHARE,

}

portfolio_sim = ska.MonteCarloSimulator(

calibration=cons.calibration.copy(),

block=cons.cons_portfolio_problem,

dr=portfolio_decision_rule,

initial={"k": Normal(mu=1.0, sigma=0.1), "R": cons.calibration["Rfree"]},

agent_count=1000,

T_sim=100,

seed=42,

)

print("\nRunning portfolio simulation...")

portfolio_sim.initialize_sim()

portfolio_sim.simulate()

print("Portfolio simulation completed successfully")

Running portfolio simulation...

Portfolio simulation completed successfully

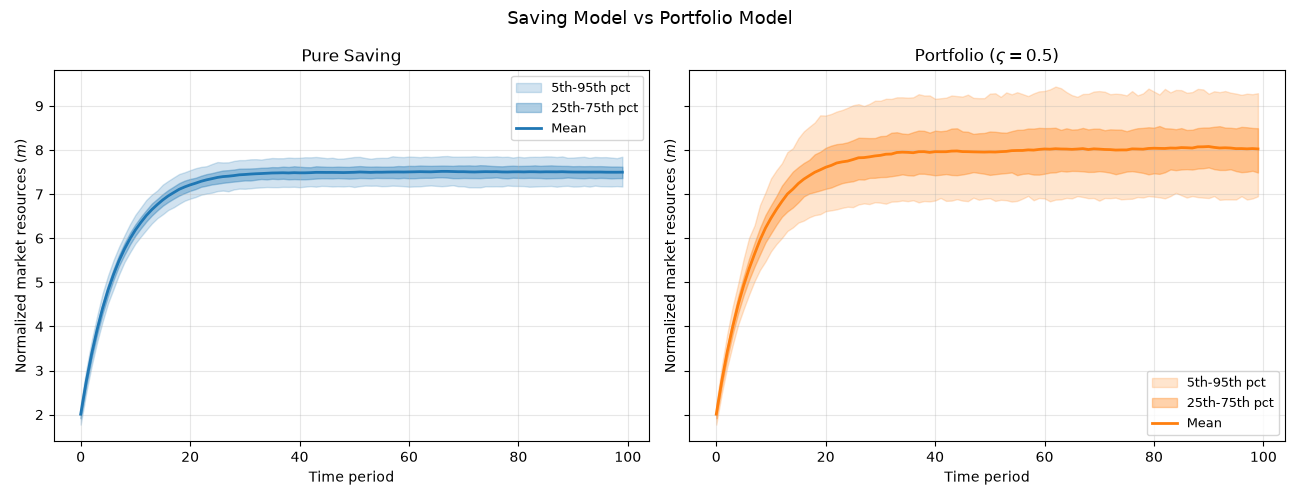

Step 8: Compare Saving vs Portfolio Paths¶

The risky asset earns a higher expected return, so the portfolio model predicts higher mean wealth accumulation - but also greater dispersion due to stock-return risk.

fig, axes = plt.subplots(1, 2, figsize=(13, 5), sharey=True)

fig.suptitle("Saving Model vs Portfolio Model", fontsize=13)

for ax, sim, label, color in [

(axes[0], simulator, "Pure Saving", "C0"),

(axes[1], portfolio_sim, rf"Portfolio ($\varsigma={RISKY_SHARE}$)", "C1"),

]:

m_h = sim.history["m"]

ax.fill_between(

range(sim.T_sim),

np.percentile(m_h, 5, axis=1),

np.percentile(m_h, 95, axis=1),

alpha=0.2,

color=color,

label="5th-95th pct",

)

ax.fill_between(

range(sim.T_sim),

np.percentile(m_h, 25, axis=1),

np.percentile(m_h, 75, axis=1),

alpha=0.35,

color=color,

label="25th-75th pct",

)

ax.plot(m_h.mean(axis=1), linewidth=2, color=color, label="Mean")

ax.set_title(label)

ax.set_xlabel("Time period")

ax.set_ylabel("Normalized market resources ($m$)")

ax.legend(fontsize=9)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Total running time of the script: (0 minutes 1.110 seconds)