Note

Go to the end to download the full example code.

Resource Extraction Model¶

The resource extraction problem models the optimal management of a renewable resource (fishery, forest, wildlife, etc.). The decision-maker must balance immediate profits from extraction against preserving the resource stock for future use.

This example implements the classic model from Reed (1979) [1], which shows that under multiplicative environmental shocks and stock-dependent harvesting costs, the optimal policy has a simple “constant escapement” form. The optimal escapement level can be computed analytically, making this an excellent benchmark for testing reinforcement learning algorithms.

Model Structure¶

State Variable: \(x_t\) — Resource stock level at time \(t\)

Control Variable: \(u_t\) — Harvest/extraction rate (constrained: \(0 \leq u_t \leq x_t\))

Dynamics¶

The resource stock evolves according to:

where:

\(r > 1\) is the deterministic growth rate

\((x_t - u_t)\) is the escapement (stock remaining after harvest)

\(\epsilon_t\) is a multiplicative environmental shock with \(\mathbb{E}[\epsilon_t] = 1\)

\(\epsilon_t\) follows a log-normal distribution: \(\ln(\epsilon_t) \sim \mathcal{N}(-\sigma^2/2, \sigma^2)\)

Profit Function¶

Single-period profit is:

where:

\(p\) is the (constant) price per unit harvested

\(c_0/x_t\) is the stock-dependent unit cost of harvesting

The cost specification captures the realistic feature that harvesting becomes more expensive when the stock is depleted (e.g., fish are harder to catch when populations are low).

Objective and Bellman Equation¶

The manager seeks to maximize expected discounted profit:

where \(\delta \in (0,1)\) is the discount factor, which reflects time preference (impatience) and risk. The Bellman equation expresses the value of being in state \(x_t\) as the maximum of current profit plus the discounted expected continuation value.

Parameters¶

\(r\) = 1.02: Growth rate (2% per period)

\(p\) = 5.0: Price per unit extracted

\(c_0\) = 10.0: Cost parameter for stock-dependent costs

\(\delta\) (DiscFac) = 0.95: Discount factor for future rewards

\(\sigma\) = 0.1: Standard deviation of log-normal growth shock

Optimal Policy: Constant Escapement¶

Reed (1979) [1] proved that the optimal policy maintains a constant target stock level \(S^*\) and harvests any surplus:

The optimal escapement level is:

This requires the “impatience condition” \(\delta r < 1\), which ensures the agent prefers extraction over indefinite accumulation.

References¶

import matplotlib.pyplot as plt

import numpy as np

import skagent as ska

from skagent.distributions import Normal

import skagent.models.resource_extraction as rex

Model Inspection¶

First, let’s load the predefined model elements and inspect them.

Step 1: Show Model Parameters¶

print("Model Calibration:")

for param, value in rex.calibration.items():

print(f" {param}: {value}")

Model Calibration:

r: 1.02

p: 5.0

c_0: 10.0

DiscFac: 0.95

sigma: 0.1

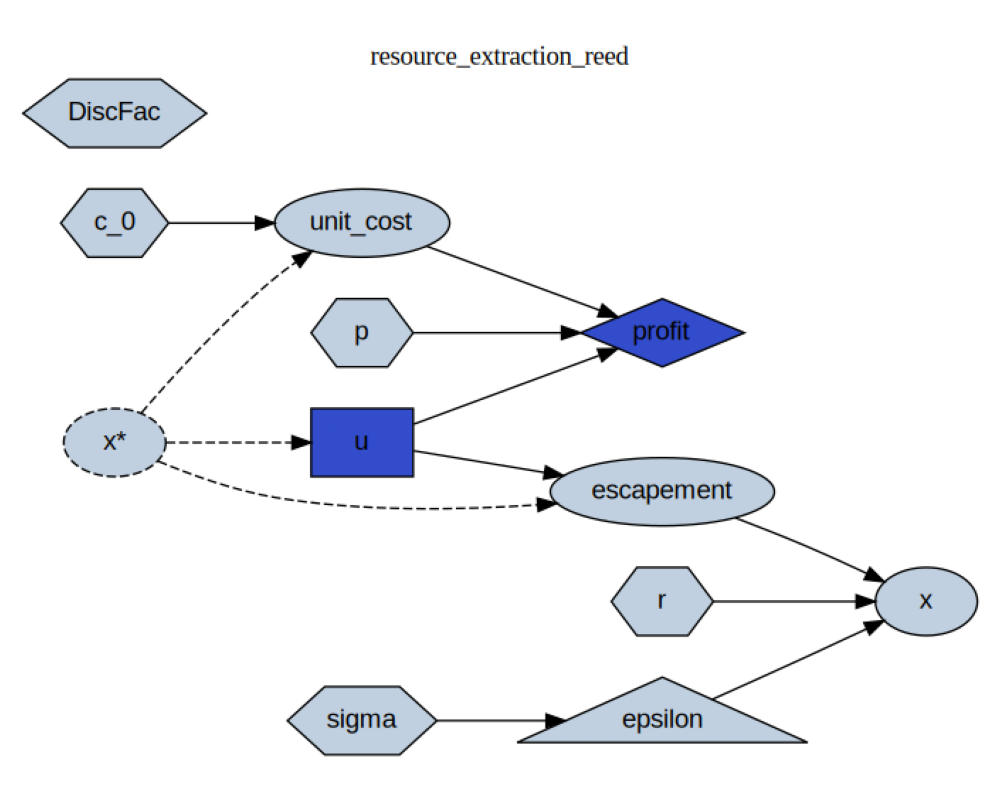

Step 2: Inspect the Resource Extraction Model¶

rex.resource_extraction_block.display_formulas()

u = Control(x)

unit_cost = lambda x, c_0: c_0 / x

profit = lambda u, p, unit_cost: (p - unit_cost) * u

escapement = lambda x, u: x - u

x = lambda escapement, r, epsilon: r * escapement * epsilon

Step 3: Visualize the Resource Extraction Model¶

img, _ = rex.resource_extraction_block.display(rex.calibration)

plt.figure(figsize=(10, 8))

plt.imshow(img)

plt.axis("off")

plt.tight_layout()

<IPython.core.display.SVG object>

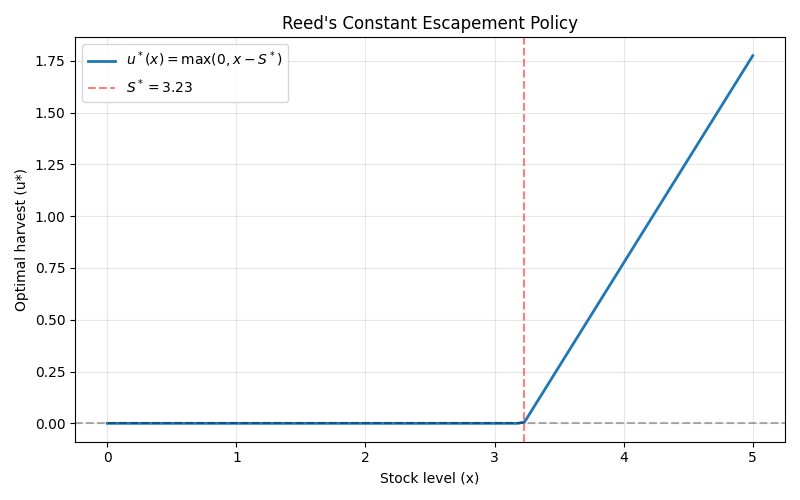

Step 4: Compute Optimal Escapement Policy¶

Reed (1979) proved that the optimal policy has a constant escapement form:

where \(S^*\) is the optimal escapement level (target stock to maintain).

The optimal escapement can be computed analytically:

This analytical solution makes the model ideal for validating reinforcement learning algorithms—we can compare learned policies against the known optimum.

dr_u, _ = rex.make_optimal_decision_rule(rex.calibration)

# Compute S* for display

r = rex.calibration["r"]

p = rex.calibration["p"]

c_0 = rex.calibration["c_0"]

delta = rex.calibration["DiscFac"]

S_star = c_0 * (1 - delta) / (p * (1 - delta * r))

print(f"\nOptimal escapement level: S* = {S_star:.4f}")

print(f"Optimal policy: u*(x) = max(0, x - {S_star:.4f})")

# Visualize the policy

x_range = np.linspace(0, 5, 100)

u_optimal = dr_u(x_range)

plt.figure(figsize=(8, 5))

plt.plot(x_range, u_optimal, label=r"$u^*(x) = \max(0, x - S^*)$", linewidth=2)

plt.axhline(y=0, color="k", linestyle="--", alpha=0.3)

plt.axvline(

x=S_star, color="r", linestyle="--", alpha=0.5, label=f"$S^* = {S_star:.2f}$"

)

plt.xlabel("Stock level (x)")

plt.ylabel("Optimal harvest (u*)")

plt.title("Reed's Constant Escapement Policy")

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

# Wrap rules in the format expected by simulator

decision_rule = {"u": dr_u}

Optimal escapement level: S* = 3.2258

Optimal policy: u*(x) = max(0, x - 3.2258)

Step 5: Run Monte Carlo Simulation¶

# Initial conditions - start with stock level around 2*S*

initial_conditions = {

"x": Normal(mu=2 * S_star, sigma=0.1),

}

# Create and run simulator

simulator = ska.MonteCarloSimulator(

calibration=rex.calibration,

block=rex.resource_extraction_block,

dr=decision_rule,

initial=initial_conditions,

agent_count=1000, # Simulate 1000 agents

T_sim=100, # For 100 periods

seed=42, # For reproducibility

)

# Run the simulation

print("\nRunning simulation...")

simulator.initialize_sim() # Initialize simulation variables

simulator.simulate()

print("✓ Simulation completed successfully")

Running simulation...

✓ Simulation completed successfully

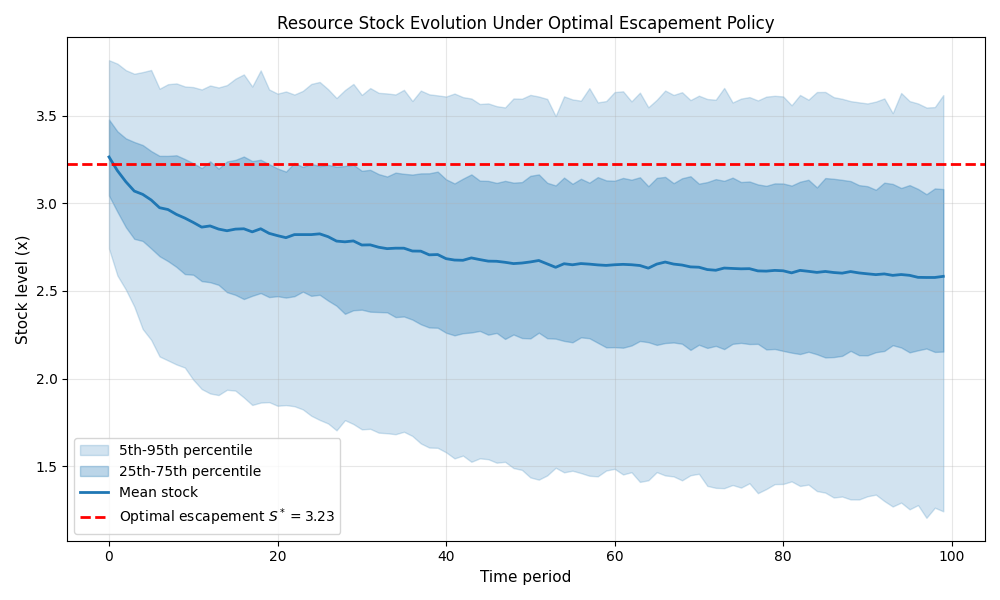

Step 6: Plot Simulation Results¶

The plot shows the distribution of stock levels over time under the optimal constant escapement policy. The stock fluctuates around \(S^*\) due to environmental shocks. When stock exceeds \(S^*\), the surplus is harvested; when shocks drive stock below \(S^*\), no harvest occurs and the stock recovers through natural growth.

plt.figure(figsize=(10, 6))

# Plot percentiles to show distribution

plt.fill_between(

range(simulator.T_sim),

np.percentile(simulator.history["x"], 5, axis=1),

np.percentile(simulator.history["x"], 95, axis=1),

alpha=0.2,

label="5th-95th percentile",

color="C0",

)

plt.fill_between(

range(simulator.T_sim),

np.percentile(simulator.history["x"], 25, axis=1),

np.percentile(simulator.history["x"], 75, axis=1),

alpha=0.3,

label="25th-75th percentile",

color="C0",

)

plt.plot(

simulator.history["x"].mean(axis=1), label="Mean stock", linewidth=2, color="C0"

)

# Add reference line for optimal escapement

plt.axhline(

y=S_star,

color="r",

linestyle="--",

linewidth=2,

label=f"Optimal escapement $S^* = {S_star:.2f}$",

)

plt.xlabel("Time period", fontsize=11)

plt.ylabel("Stock level (x)", fontsize=11)

plt.title("Resource Stock Evolution Under Optimal Escapement Policy", fontsize=12)

plt.legend(fontsize=10)

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Total running time of the script: (0 minutes 0.867 seconds)