Note

Go to the end to download the full example code.

Training a Policy Network Against a Known Solution¶

This example demonstrates scikit-agent’s neural-network training pipeline by solving a model whose optimal policy is known in closed form, then comparing the trained policy against that analytical solution. Validating a solver against a known answer is the cleanest way to build trust in it before applying it to models that have no closed form.

The model: normalized permanent-income consumption (U-2)¶

The U-2 benchmark is a normalized version of the permanent-income hypothesis

(PIH) consumption-savings problem. It is one of the analytic benchmarks in

skagent.models.benchmarks; that module’s registry holds the full block

definition, the calibration, and the closed-form policy

(get_analytical_policy()) used as the target

below. Working in ratios to permanent income, the state is normalized assets

\(a\), the within-period resource is cash-on-hand

\(m = R a / \psi + 1\), and the control is normalized consumption

\(c\). The agent solves

with constant-relative-risk-aversion utility \(u\) and discount factor \(\beta\). For this calibration the optimal policy is affine in cash-on-hand,

where both the marginal propensity to consume \(\kappa = 1 - \beta\) and the normalized human wealth \(h = 1/r\) have closed forms. At this calibration \(h = 1/0.03 \approx 33.3\), so the intercept \(\kappa h\) dominates and the consumption function is nearly flat over the training range. This gives us an exact target to check the trained policy against.

Why a value head: the level-identification problem¶

A policy trained only on the Euler equation

\(u'(c_t) = \beta R \, \mathbb{E}[u'(c_{t+1})]\) pins down the slope of

the consumption function but not its level: scaling the whole policy leaves

the Euler residual nearly unchanged. A

BlockPolicyValueNet resolves this indeterminacy: it

shares one hidden backbone between a policy head and a value head, training them

together under a single optimizer with

BellmanEquationLoss. The value head anchors the level

through the Bellman equation \(V(m) = u(c) + \beta \mathbb{E}[V(m')]\),

which pins down what the Euler equation alone leaves free.

Why we re-sample the states¶

The single most important ingredient for accuracy is that the training states

are re-sampled on every gradient step, not fixed once. Maliar, Maliar, and

Winant (2021) keep the data “constantly re-sampled during training,” and it

matters: on a fixed handful of points the network drives those points’

residuals to zero while the consumption level drifts between them, and the

error stalls at several percent (and worsens with more epochs). Drawing a fresh

batch each step instead enforces the residual across the whole domain, which

pins the level and lets the error fall below one percent. The per-step optimizer

is train_block_nn(); the loop in Step 4 supplies the fresh

states and threads Adam’s momentum through. The loss combines the MMW’21

all-in-one expectation operator (two independent shock copies per state) with

the Bellman first-order-condition term.

A complementary ingredient of the full MMW’21 algorithm, simulating the model

forward so the sampled states concentrate on the ergodic set, is provided by

maliar_training_loop(); for a worked demonstration

on a model with no closed-form solution, see the companion gallery example

plot_maliar_training_loop.py.

import matplotlib.pyplot as plt

import numpy as np

import torch

import skagent.bellman as bellman

import skagent.grid as grid

import skagent.loss as loss

from skagent.ann import BlockPolicyValueNet, device, train_block_nn

from skagent.models.benchmarks import (

get_analytical_policy,

get_benchmark_calibration,

get_benchmark_model,

)

SEED = 10077693

Step 1: Load the U-2 benchmark and build a BellmanPeriod¶

get_benchmark_model returns the model block; get_analytical_policy

returns the closed-form solution we will validate against.

u2_block = get_benchmark_model("U-2")

u2_calibration = get_benchmark_calibration("U-2")

analytical_policy = get_analytical_policy("U-2")

rng = np.random.default_rng(SEED)

u2_block.construct_shocks(u2_calibration, rng=rng)

bp = bellman.BellmanPeriod(u2_block, "DiscFac", u2_calibration)

Step 3: Define the Bellman-equation loss¶

BellmanEquationLoss evaluates the residual of

\(V(m) = u(c) + \beta \mathbb{E}[V(m')]\) using the network’s own value

head. foc_weight=1.0 adds the first-order-condition term (Maliar et al.

2021, eq. 14), which speeds convergence.

bellman_loss_fn = loss.BellmanEquationLoss(

bp,

pvnet.get_value_function(),

parameters=u2_calibration,

foc_weight=1.0,

)

Step 4: Train on re-sampled states, snapshotting at increasing depths¶

Accuracy hinges on re-sampling the training states on every gradient step

rather than fixing a grid (Maliar et al. 2021, who keep the data “constantly

re-sampled during training”). A fresh draw each step enforces the residual

across the whole domain; a fixed handful of points lets the network drive

their residuals to zero while the consumption level drifts between them.

Each step draws n_batch normalized-asset points with two independent

permanent-income shock copies (the all-in-one operator), and threads the

optimizer back in so Adam keeps its momentum across steps.

We evaluate the policy on a fixed grid at several training depths, so the plot can show the consumption function converging toward the analytical solution as training proceeds rather than only its final fit. The depths are checkpoints of one continuous run (the optimizer is threaded through), so snapshotting only observes training, it does not perturb it.

# Evaluation grid, held fixed across depths. The income shock is held at its

# mean so the slice is deterministic; cash-on-hand is then m = R a + 1.

n_test = 50

test_a = torch.linspace(0.5, 5.0, n_test, device=device)

test_states = {"a": test_a}

test_shocks = {"psi": torch.ones(n_test, device=device)}

test_m = (u2_calibration["R"] * test_a / test_shocks["psi"] + 1.0).cpu().numpy()

def consumption_on_test_grid(net):

decision_fn = net.get_decision_function()

c = decision_fn(test_states, test_shocks, u2_calibration)["c"]

return c.detach().cpu().numpy()

n_batch = 256

checkpoints = [100, 500, 1500, 5000] # cumulative SGD steps to snapshot at

snapshots = {}

optimizer = None

final_loss = float("nan")

step = 0

for target in checkpoints:

while step < target:

train_grid = grid.Grid.from_dict(

{

"a": torch.empty(n_batch, device=device).uniform_(0.5, 5.0),

"psi_0": torch.ones(n_batch, device=device),

"psi_1": torch.ones(n_batch, device=device),

}

)

pvnet, final_loss, optimizer = train_block_nn(

pvnet,

train_grid,

bellman_loss_fn,

epochs=1,

lr=1e-3,

optimizer=optimizer,

verbose=False,

)

step += 1

snapshots[target] = consumption_on_test_grid(pvnet)

trained_net = pvnet

print(f"Final training loss: {final_loss:.3e}")

Final training loss: 3.487e-06

Step 5: Compare the deepest-trained policy to the analytical solution¶

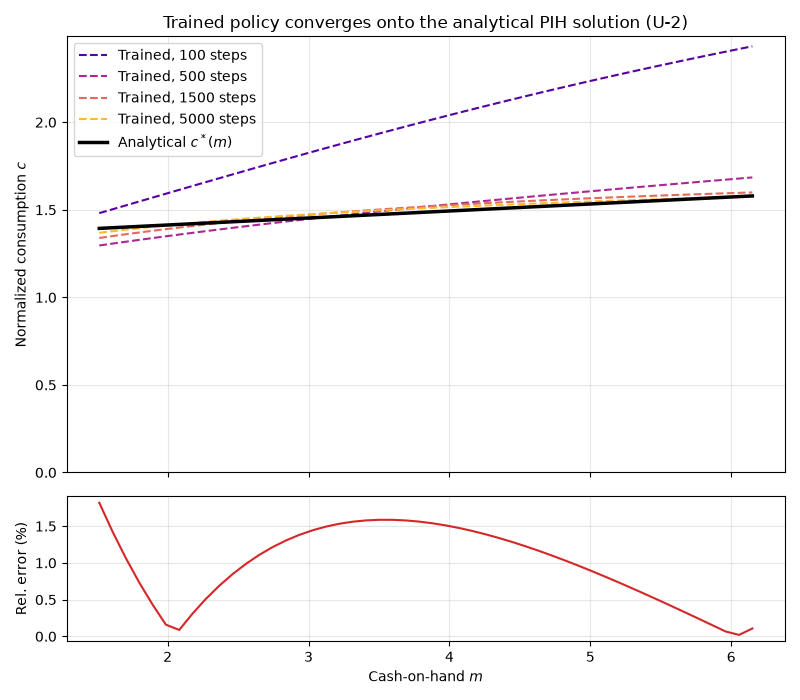

At the deepest snapshot we report the pointwise relative error against the closed-form policy. With re-sampled training and the value head anchoring the level, the mean relative error falls to about one percent (here 0.98%), an order of magnitude tighter than the several-percent floor of Euler-only training on this unconstrained model.

analytical_np = (

analytical_policy(test_states, test_shocks, u2_calibration)["c"]

.detach()

.cpu()

.numpy()

)

trained_np = snapshots[checkpoints[-1]]

rel_error_np = np.abs(trained_np - analytical_np) / (analytical_np + 1e-8)

print(f"Mean relative error: {rel_error_np.mean():.2%}")

print(f"Max relative error: {rel_error_np.max():.2%}")

Mean relative error: 0.98%

Max relative error: 1.82%

Step 6: Plot the policy converging onto the analytical solution¶

Consumption is a function of cash-on-hand m, so we plot against m (not assets a), and start the consumption axis at 0 so the level is shown honestly. Each dashed curve is the trained policy after a given number of SGD steps: as training deepens the curves march onto the closed-form linear PIH rule, making it visible that the error keeps shrinking with training rather than stalling. The lower panel shows the pointwise relative error at the deepest snapshot.

fig, (ax_policy, ax_err) = plt.subplots(

2, 1, figsize=(8, 7), sharex=True, height_ratios=[3, 1]

)

depth_colors = plt.cm.plasma(np.linspace(0.15, 0.85, len(checkpoints)))

for color, steps in zip(depth_colors, checkpoints):

ax_policy.plot(

test_m,

snapshots[steps],

"--",

color=color,

linewidth=1.5,

label=f"Trained, {steps} steps",

)

ax_policy.plot(test_m, analytical_np, "k-", linewidth=2.5, label="Analytical $c^*(m)$")

ax_policy.set_ylabel("Normalized consumption $c$")

ax_policy.set_ylim(bottom=0.0)

ax_policy.set_title("Trained policy converges onto the analytical PIH solution (U-2)")

ax_policy.legend()

ax_policy.grid(True, alpha=0.3)

ax_err.plot(test_m, rel_error_np * 100.0, "C3-", linewidth=1.5)

ax_err.set_xlabel("Cash-on-hand $m$")

ax_err.set_ylabel("Rel. error (%)")

ax_err.grid(True, alpha=0.3)

fig.tight_layout()

plt.show()

Total running time of the script: (0 minutes 24.759 seconds)